Under Form 10BD, Charitable Institution has to report the Total Donation received during the Financial year with the particulars of each donor’s Details such as PAN, Name, Address, Purpose of Donation and mode of Donation. Experts has a view that the total amount of Donation booked and declared in the Income and statement accounts must tally with the total figures.

Following Details of the donors and their donation is to be filled as per the CBDT Notification No51/2022 dated 9th May 2022.

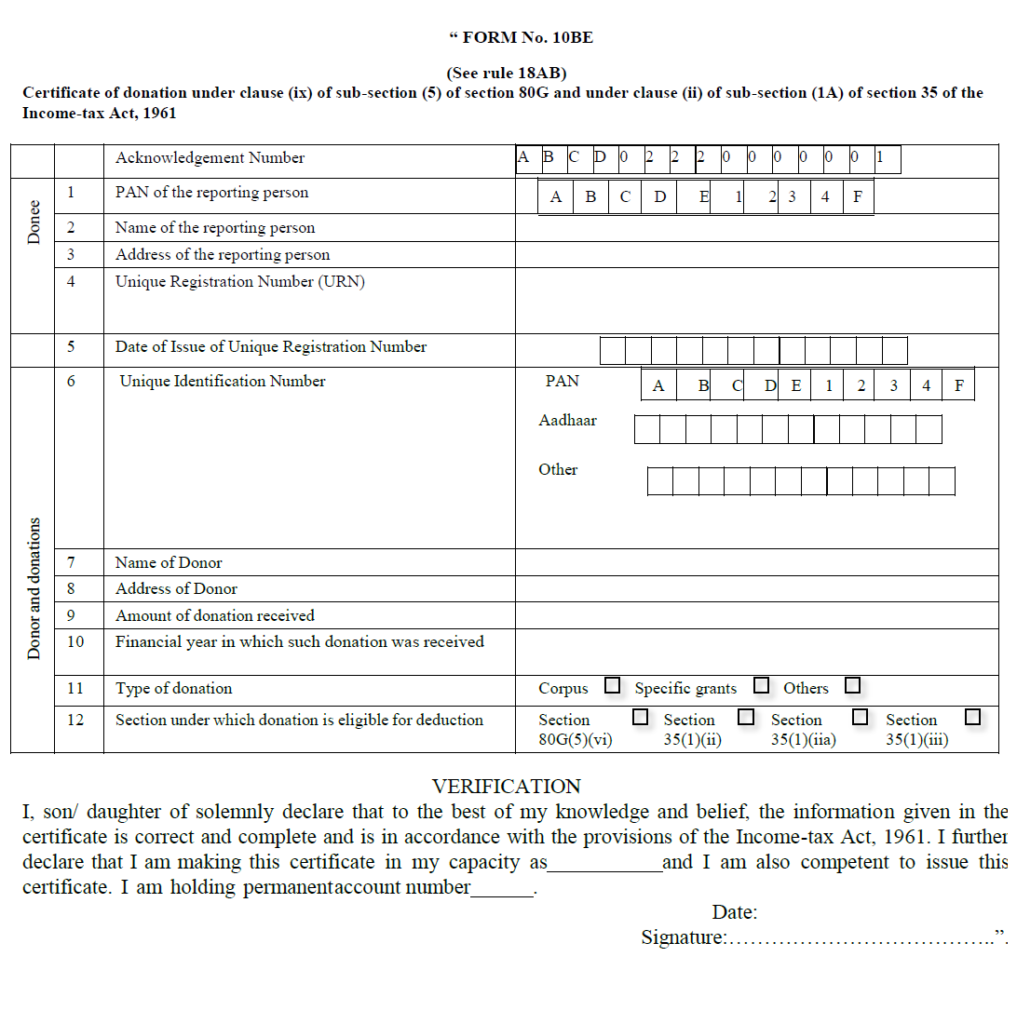

After Successful submission, Portal will generate the Form 10BE which is nothing but a certificate of Donation which should be awarded to the Donor by the Charitable Institution. This will come with a unique Acknowledgement Number as will be a valid proof to claim deduction under section 80G for the Donor.

Following are the particulars of the Form 10BE as per the CBDT Notification No51/2022 dated 9th May 2022.